The year 2021 was phenomenal for stock market investors in many ways. The benchmark indices skyrocketed. Most sectoral and thematic indices were also raging as the economic recovery was well within sight. The retail participation also saw remarkable growth – Mutual Fund folios, Demat accounts, and retail inflows all jumped exponentially.

Must Read – What is Equity?

The companies waiting for a bull run to float their public issues could not have a better opportunity. IPOs were literally raining in 2021. Every time it felt like it is enough, the primary markets and listing gains surprised us all. Many records shattered in 2021.

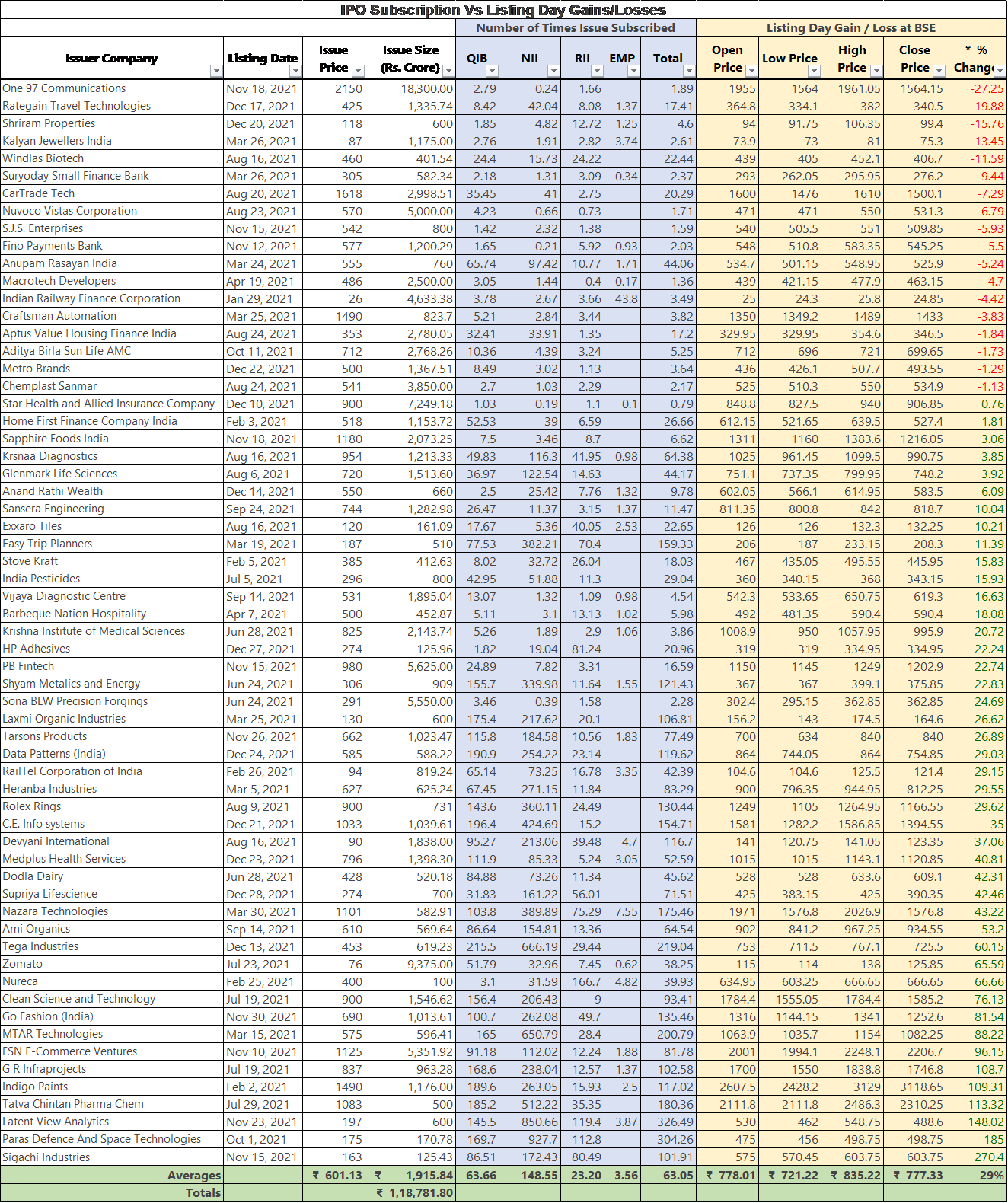

- The largest-ever IPO by PayTM at ₹18,300 crores. A record broken after 11 years when Coal India garnered ₹15,200 crores in 2010.

- Total funds raised crossed the mythical ceiling of 1 lakh crore at ₹1.18 lakh crores. 72.5% higher than the last record of ₹68,827 crores set in 2017.

- IPO oversubscription stood at an average of 63x.

- 62 companies hit the market and were listed in 2021. If you count all IPOS listed in 2021, the number goes to 65.

The stock market on steroids presents an excellent environment for promoters to raise capital from the public.

But are the sky-high valuations justifiable from an investors’ point of view?

Should you invest in the mega IPO of LIC?

What about the IPOs of Delhivery, Droom, MobiKwik, Oyo, Pharmeasy, Ixigo, BYJU’S, and Foxconn India’s unit Bharat FIH Ltd lined up for 2022?

The headlines are screaming:

- Average 29% listing gain. 44 out of 62 IPOs closed higher on listing than their issue price.

- India is at the cusp of the multi-year bull run. Sensex to cross 75,000 in 2022.

- Domestic retail investors are driving the rally. FPIs do not matter.

- THIS TIME IT IS DIFFERENT.

If you base your investment decisions solely on such headlines, then certainly, go ahead and invest in the IPOs of LIC and other companies. Plenty of articles, talk shows, and investment gurus will nudge, nay push, you to ‘invest’ in these IPOs for listing gains.

But there is more to IPOs than just listing gains and quick bucks. Let us unravel some myths before you go all in.

6 Myths about IPO everyone Should know before investing in LIC IPO

Myth 1: More Data Means Better Information

When a well-known and trusted brand like the LIC comes for a public listing, the information about its operations, profitability, and market leadership is blasted from all corners. The media buildup – sponsored (in case of fishy IPOs) or organic (like in case of LIC) – can make it hard to ignore the company or its IPO.

This frenzy can confuse an investor and an IPO application seems to be the sure shot golden ticket to riches. Before investing in new IPOs just recall the frenzy created by the Reliance Power IPO in late 2007 and early 2008. It was the biggest ever IPO to date with the highest number of subscriptions. Yet the day it was listed the Indian stock markets crashed. The same thing repeated with PayTM in November 2021, albeit it was not a total disaster like Reliance Power.

Check 2010 Post – IPO Mania

Myth 2: Public Excitement Means Better Prospects

Sometimes a well-liked brand or company can still be a bad investment. What would you say about the State Bank of India? SBI is India’s largest bank by the number of customers, accounts, loans, balance sheet, branches, ATMs – take any parameter for that matter. But by market capitalization, HDFC Bank is India’s top lender at ₹8.2 lakh crores. The SBI, which is thrice the size of HDFC Bank in most respects, has a market valuation that is just half of its private rival at ₹4.1 lakh crores!

Even after the current bull run, among the top 100 companies in India, only 7 are PSUs directly, and 5 indirectly (including SBI Life, SBI Cards, and IDBI, Axis & IndusInd Banks – having a major/significant shareholder as another PSU/Government). If you leave out SBI, there is NO other PSU bank in the top 100 companies, out of 12 listed PSU banks! This tells something about the management by the government.

Myth 3: IPO Always Give Higher Returns

Not necessarily. Newly listed companies do not have a proven track record of performance and therefore are categorized as high-risk investments. Historical data points that almost all wealth is cornered by the sellers in an IPO and none by the buyers.

Warren Buffett has said, “It’s almost a mathematical impossibility to imagine that, out of the thousands of things for sale on a given day, the most attractively priced is the one being sold by a knowledgeable seller (company insiders) to a less-knowledgeable buyer (investors)”.

Benjamin Graham, the guru of Warren Buffet, said, “Intelligent investors should conclude that IPO stands for Initial public offering. More accurately it is also a shorthand for – It’s Probably Overpriced, or Imaginary Profits Only, or even Insiders Private Opportunity”.

Ask yourself this: When would you be willing to sell your house/gold? When you can fetch the maximum price for it or when it is “fairly” priced?

Must Check- How you benefit from long term orientation in Life and in Investing

Myth 4: A Company Going Public Is Financially Stable

The stability of a company depends on many factors. Stability on books cannot ensure if it will continue to grow, remain/become profitable, remain stable, or even solvent, after listing.

Many factors are beyond management control. Any black-swan event – like COIVD-19 – can disrupt all their plans and put the future of the company in jeopardy. We are not saying the LIC is or can become unstable. But are we only talking about the LIC IPO? Certainly no. For example, BYJU’s is being called out for its questionable sales practices and service and might face regulatory action in the future.

Myth 5: All Retail Investors Get Allotment

- The only priority accorded to retail investors is the 35% quota. In the case of the LIC IPO, policyholders might also get a special quota to participate in the IPO.

But if the above table is anything to go by, then on average 23.2 retail investors applied for 1 share. It means only one out of 24 investors will get an allotment. If the IPO is oversubscribed many times over, then a lottery system is used to allocate lots to retail investors. The pro-rata allotment is no longer applied, but the one-lot-to-each investor is followed.

Myth 6: I can Participate in Company’s Future Growth

Before they go public, most companies receive some rounds of private investments. The VCs got the first access to the pie while it was affordable. Most IPOs are a mechanism for promoters and VCs to offload their stake on retail investors when the momentum is already tapering.

If you assume that the trajectory of the share price after an IPO will always be upwards, then you are in for a rude shock. Many companies never, or rarely, cross their issue price. PayTM is one example. However, its history is too short, but the most recent and well-known. Similarly, once Coal India slipped below its listing price in Late 2019, it has never recovered!

Read – 5 Things You Should Know About Risk and Your Investments

Why Avoid All IPOs? or Should I invest In LIC IPO

The frenzy, cheerleading, blitz, and euphoria that follows a bull run and leads the IPO run, can deafen and blind you. As a responsible investor, you must filter noise and keep a cool head. Do not get seduced by the ‘hotness’ of the stock and heed the advice of the father of value investing.

Benjamin Graham, in his famous book The Intelligent Investor, states, “An elementary requirement for the intelligent investor is an ability to resist the blandishments of salesmen offering new common stock issues during bull markets. Some of these issues may prove excellent buys – a few years later when nobody wants them.”

He goes on to prophesize, “Somewhere in the middle of a bull market, the first new issues make their appearance. These are priced not unattractively and some large profits are made by the buyers of the early issues.

As the market continues to rise, this brand of financing goes more frequent; the quality of the companies steadily poorer; the prices asked verge on the exorbitant.

One fairly dependable sign of the approaching end of a bull swing is the fact that new issues of small and nondescript companies are offered at prices somewhat higher than the current level for many mediums sized companies with long market history.”

Investing is one of the most lonesome professions, and by following the herd you may end up in a ditch or the belly of a predator. IPOs can be luring but so are the predators from the animal kingdom who lure their prey. Lurers can employ active or passive luring strategies. They can turn on or off their deceptive signals (sponsored media blitz) or lure only when environmental conditions are appropriate (a bull run).

As most of the retail investors in India are new to equity investing, it is not hard to deceive them. As most of the IPOs come during a sustained bull run, it is most likely there is nothing left on the table for retail investors to benefit from.

If the investors are not alert and mindful, then they can fall prey to such predators.

If you are still convinced that the LIC IPO, or any other IPO, should be part of your portfolio to meet specific goals, then you can always buy them on listing. Alternatively, you can invest in Mutual funds that are anchor investors in that IPO and diversify your risks.

The entire article can be summed up in just one phrase commonly used in Contract Laws – Caveat Emptor or Buyer Beware.

On a lighter note full form of IPO is – It’s Probably Overpriced. 😜

Please share your views or experience of investing in IPOs.

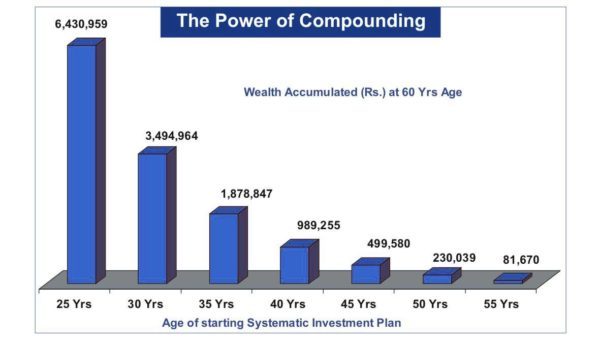

As someone rightly said, “Journey of Thousand miles starts with a little step”. Make sure that you start your SIP for your long-term financial goals today.

As someone rightly said, “Journey of Thousand miles starts with a little step”. Make sure that you start your SIP for your long-term financial goals today.

Must Read –

Must Read –

6. Interest Rate Risk

6. Interest Rate Risk