There is a saying that ” an apple a day, keeps the doctor Away…” but this does not apply in today ‘s world . First of all, not everyone can afford to have an apple a day and even if people who can afford, eat impure apples, get sick and then meet doctors. End of the day, we meet doctors more regularly even more than we meet our near dear ones. Do some calculations on your own and find out, how much money you spend on monthly basis just to visit doctor, buying medicine and getting the RECOMMENDED test done. Don’t take into account any hospitalization cost you incurred, else you may well have a high BP.

There is a saying that ” an apple a day, keeps the doctor Away…” but this does not apply in today ‘s world . First of all, not everyone can afford to have an apple a day and even if people who can afford, eat impure apples, get sick and then meet doctors. End of the day, we meet doctors more regularly even more than we meet our near dear ones. Do some calculations on your own and find out, how much money you spend on monthly basis just to visit doctor, buying medicine and getting the RECOMMENDED test done. Don’t take into account any hospitalization cost you incurred, else you may well have a high BP.

Read – Best medical insurance for parents

India Vs USA

Bottom line, The medical expenses are increasing day by day, there is no escape to this. You will be astonished to know that in US, 15% US GDP is all spent on medical cost. 15 % of US GDP means, close to double of India GDP which is over Rs. 5,60,000 Crore. In US 15.3% population is not insured by health cover & another 35% of the population is under insured but in India 88% of the population is not covered by health insurance. Medical expense are now on the rise in India as well. In today ‘s fast moving and fast earning life, we spent our half working life in 5 star hotels and half in 5 star hospitals. There lies a huge risk with everyone about medical cost hitting ones finances in such a bad way, that at times, it is beyond repairable. We meet many people who sell even their house/gold or withdrawing from retirement savings just to cover the medical cost. In such a scenario, one has to cover themselves from such a risk and get a good Medical cover in the form Mediclaim policy.

Check – Health insurance portability

What Mediclaim Policy covers

Mediclaim policy covers against hospitalization cost one incur, provide one is admitted for more than 24 hours. It covers various cost during hospitalization including that of medication, surgery, room cost, ambulance etc. It also covers the cost you incur on medication, test, doctor’s fees etc. 30 days and 60 days post hospitalization provided the cost is incurred for the same cause for which one is hospitalized.

Mediclaim policy covers against hospitalization cost one incur, provide one is admitted for more than 24 hours. It covers various cost during hospitalization including that of medication, surgery, room cost, ambulance etc. It also covers the cost you incur on medication, test, doctor’s fees etc. 30 days and 60 days post hospitalization provided the cost is incurred for the same cause for which one is hospitalized.

Who provide Mediclaim policies

Mediclaim Policy is typically offered by General Insurance Companies & health insurance cos. both in public domain. There are many life insurance companies that also offers such similar products but it is better to take policy from specialist.

Read: The rising strength of Indian Middle Class

Type of Mediclaim Policies

Predominantly there are two types of medical policy available. The most common way of taking such policy is where, you buy a specific coverage called sum assured for each of the family members for which you want the cover(Individual Plan). The other way of taking the policy is that you buy a sum assured not specific to any particular person in the family but for the whole family, this is known as Floater Policy(Family Plan).

For example, a family of four, husband, wife and 2 kids. One may take Rs. 1 Lac cover for each of the person and if any one meets with casualty and is hospitalized, the insurer will pay up to the limit specific to the person. But if you have taken a floater policy, you buy a float cover, let say of up to Rs. 3 lacs for the entire family. Now if anyone in the family, meets with casualty, the cover is up to Rs 3 lacs. But if one has fully used that float, then for that year, insurance company will not pay anything if either the same person or someone else family incurs hospitalization cost.

Special policies for senior citizens are also available. Consult a Certified Financial Planner near you before taking the policy because it’s important to first judge your requirement & then select best suitable policy.

Also Read: How much medical insurance I need

Claim settlement process

There is a myth that taking claim from insurance companies is to difficult. Yes, it is, if you are not aware of methodology and at times, many people file claim for something which they are not covered for or not informing insurer at the time of hospitalization(in case of cashless claims). The system is such that most of the insurance company has a TPA (Third Party Administrator), TPA is an outsourcing agency of Insurance companies that services claims. Once the policy is taken, insurance company issues card to the Policy holder with name of TPA on it. Policy holder have freedom to select it from list of TPAs with insurance company. In case, one meets with casualty, he/she has to produce the same card in hospital. Earlier, there was a system of reimbursement of expense where in you first spend the money from your pocket and then apply for claim. Now, TPA offers CASHLESS arrangements with many hospitals. if you get admitted such hospitals, the TPA would directly make payment for which you are entitled and hence there is no problem of you arranging Cash immediately.

Tax Benefits on Medicalim Policies

Mediclaim Policy offers tax benefit as well under section 80(D) when premium is paid by any mode other than cash. A person who is 30% tax slab can income tax upto Rs 12360 by paying Rs 40000 as premium. Check Table:

Users of financial products make costly mistakes, either they buy costly life insurance policy or they ignore cheap Mediclaim Policy and then incur huge cost. Choice is yours.

Users of financial products make costly mistakes, either they buy costly life insurance policy or they ignore cheap Mediclaim Policy and then incur huge cost. Choice is yours.

Read More Articles on Insurance.

Please add your comments: Your comments will help us to write better in future.

‘Keep it Simple Stupid’ phrase is mostly used in Management Books where it is taught that the more simpler the solution would be, the more effectiveness it will have. Management is nothing but techniques that should be used in day to day life. Even in case of Financial Matters this rule of Management applies.

‘Keep it Simple Stupid’ phrase is mostly used in Management Books where it is taught that the more simpler the solution would be, the more effectiveness it will have. Management is nothing but techniques that should be used in day to day life. Even in case of Financial Matters this rule of Management applies.

This financial year has come with some changes which would affect our personal financial in some way or the other. In this article we would like to highlight changes that are made in the interest that you get in your savings bank account, PPF account and also about PAN card regulation as far as your deposits are concerned. Let’s discuss these changes one by one:

This financial year has come with some changes which would affect our personal financial in some way or the other. In this article we would like to highlight changes that are made in the interest that you get in your savings bank account, PPF account and also about PAN card regulation as far as your deposits are concerned. Let’s discuss these changes one by one:

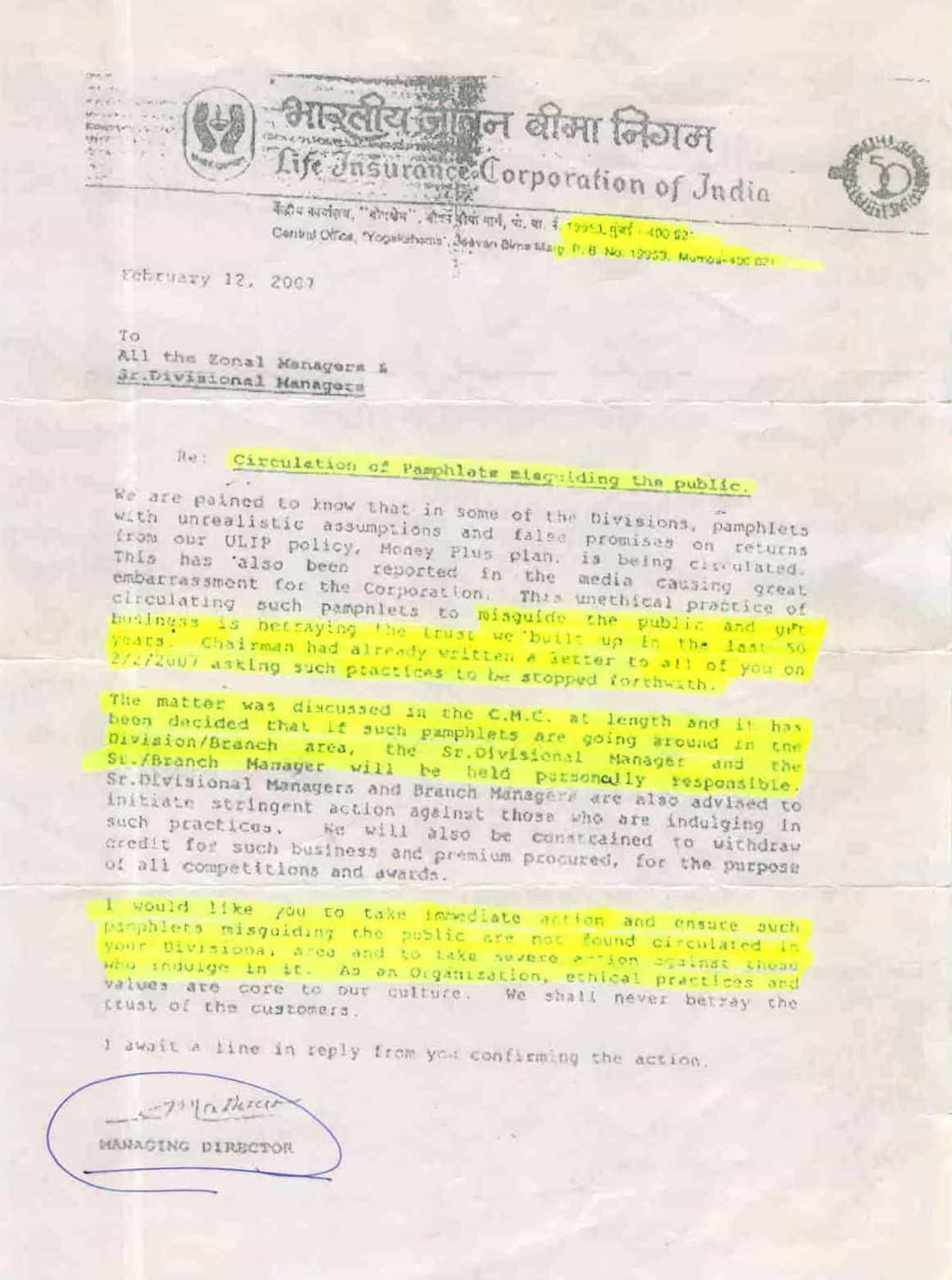

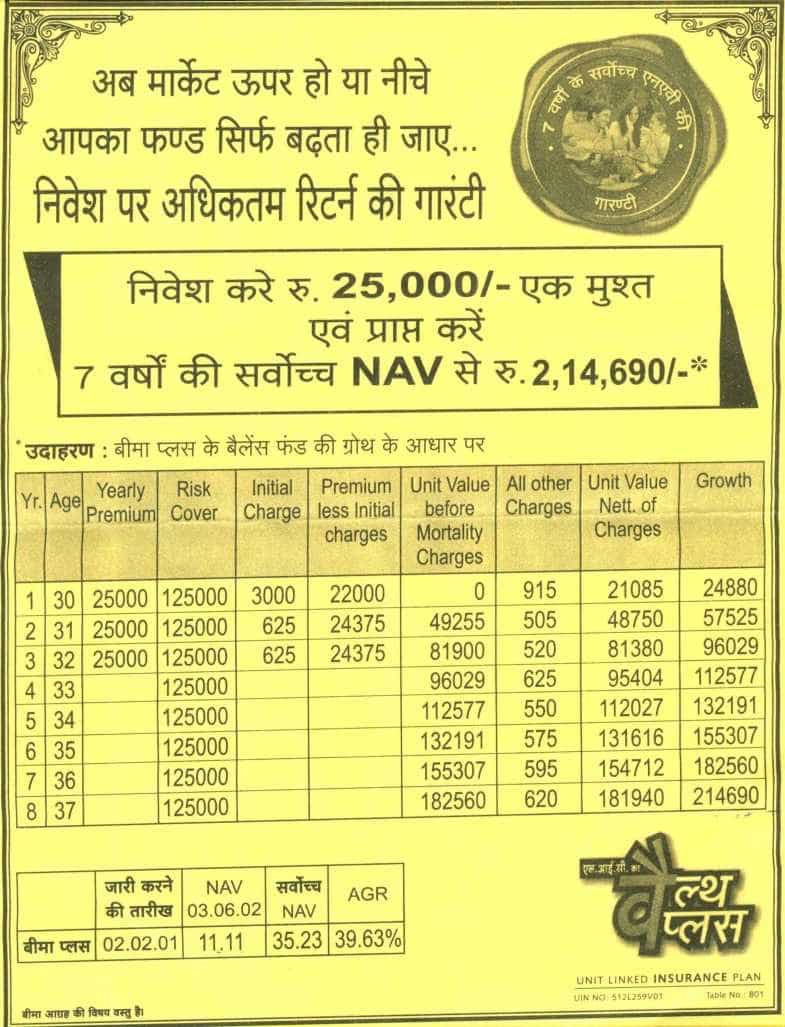

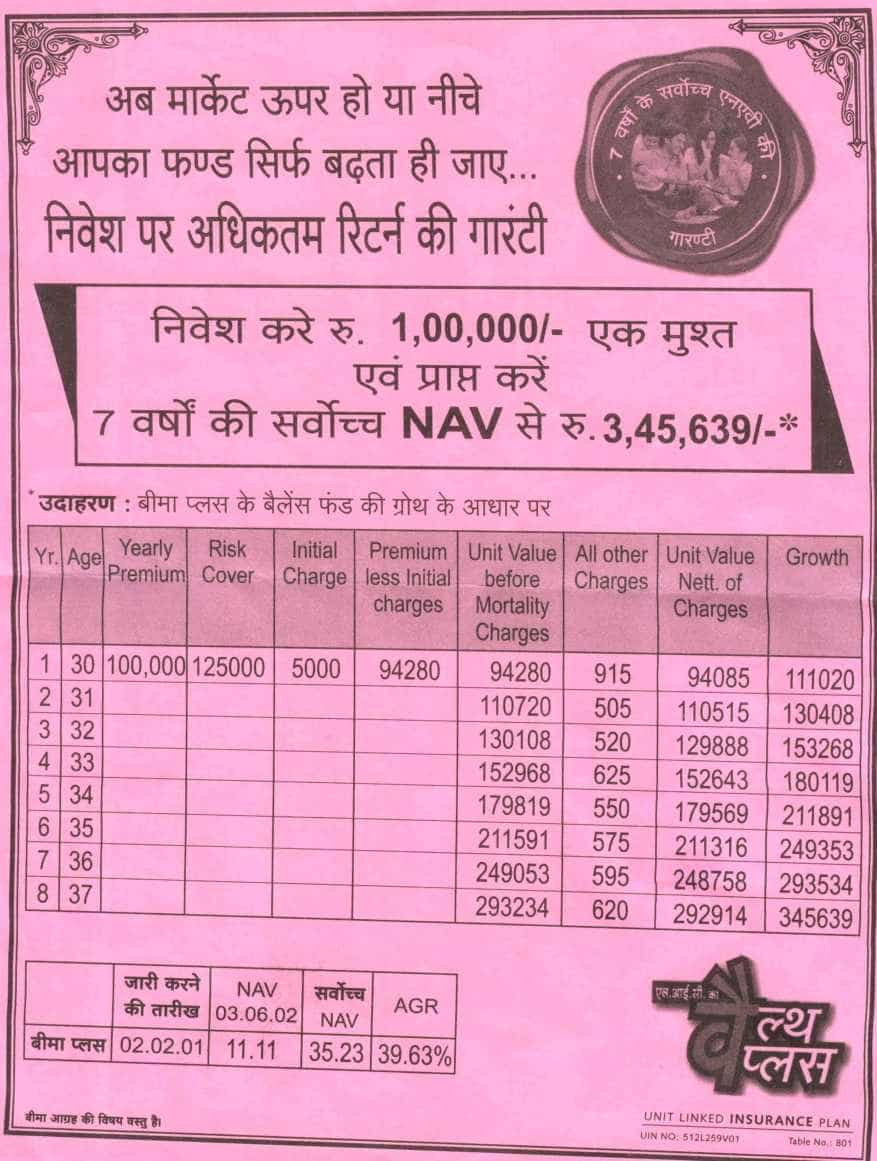

On Sunday morning when people got up and read news papers, many got a shock of their lives and many were worried as well. Not that any calamity happen nor government raised any taxes. The news was “Banning of ULIPs” which made investor worried about their investments in various ULIPs which they were sold under some obligation or by

On Sunday morning when people got up and read news papers, many got a shock of their lives and many were worried as well. Not that any calamity happen nor government raised any taxes. The news was “Banning of ULIPs” which made investor worried about their investments in various ULIPs which they were sold under some obligation or by

We at TFL, are working constantly on Investor Education and following different ways and means through which our message could be reached to as many people as possible.

We at TFL, are working constantly on Investor Education and following different ways and means through which our message could be reached to as many people as possible.